Construction Industry Monthly Snapshot by Barbour ABI

A monthly snapshot of the UK construction industry covering contract awards, planning approvals, and applications by sector, featuring expert commentary and detailed data visualisations.

Construction Industry Monthly Snapshot - April 2026⬇️

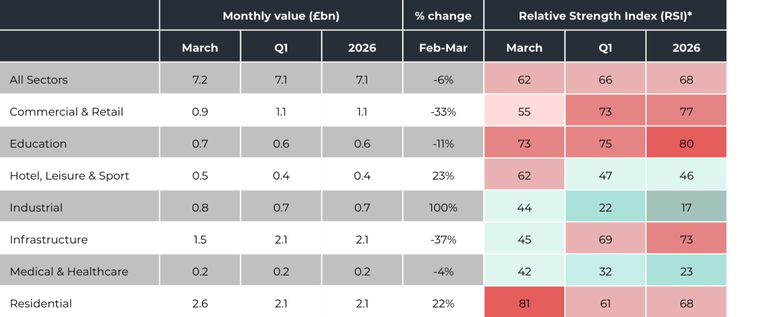

Contract Awards

Contract awards totalled £7.18bn in March, a modest softening on February’s elevated level but broadly aligned with the steady momentum seen across Q1.

Activity remained well‑distributed, with Residential retaining the largest share of monthly value, supported by a wide mix of major estate redevelopments, large housing phases and substantial volumes of student and care accommodation.

Residential awards reached £2.57bn in March, underpinned by high-value schemes such as Penvose Student Village (£148m), and a series of significant London projects including Selby Urban Village (£120m) and City Link House, Addiscombe Road (£105m).

Regionally, London led contract awards with £1.55bn, driven by a concentration of large Residential, Industrial and Infrastructure projects. The North West (£0.97bn) and South West (£0.82bn) also had strong months, the former boosted by industrial and medical schemes and the latter by airport upgrades and large educational and residential projects. The North East (£0.38bn) posted one of the sharpest rebounds month on month (c.+49%), reflecting major Infrastructure and Leisure investment.

Contract Award Monthly Value by Sector (£bn)

No Data Found

Region Share of Award Value by Sector (%)

No Data Found

Monthly Highlights

- Industrial activity grew sharply month on month, reaching £0.80bn, driven by a cluster of large logistics and manufacturing schemes. Notable awards included the Panattoni Hardwick Grange industrial building (£135m), Bredbury Employment Park (£70m) and multiple logistics hubs, factory expansions and warehousing schemes across the Midlands, North West and Scotland.

- Hotel, Leisure & Sport awards climbed to £0.50bn, reflecting a significant uplift from earlier in the year. The standout project was the Crystal Palace National Sports Centre redevelopment (£130m), alongside major hotel projects in Scotland (£94m), West Midlands (£28m), and North East (£28m). A broad base of community and sports facility improvements contributed to depth within the sector.

- Infrastructure awards moderated to £1.52bn, down from February but still reflective of strong sectoral structural demand. The month was dominated by energy transition assets — including the Longfield 500MW Solar Farm (£350m) and major port, rail and airport upgrades. The mix featured battery storage, large scale solar, flood defence works, public realm highways improvements and multiple hospital energy upgrades.

- Commercial & Retail awards totalled £0.90bn in March 2026, representing a moderation from February but broadly consistent with the variable month to month pattern the sector typically experiences. Activity was dominated by a combination of large office refurbishments, retail park development, logistics aligned retail, and a wide base of mid sized supermarket, drive thru and commercial space schemes across the UK.

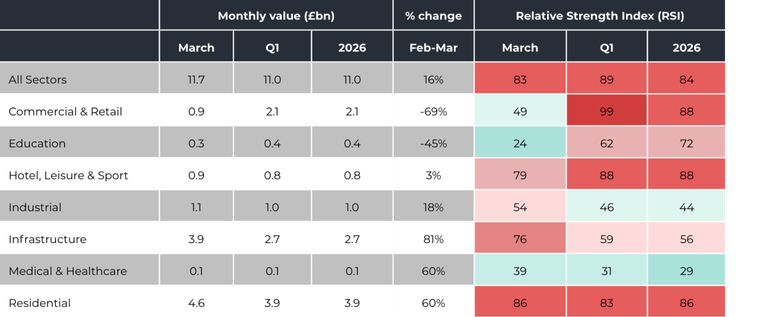

Planning Approvals

Approvals totalled £11.7bn in March 2026, reflecting a stable upswing from February’s softer performance and marking a continuation of the elevated activity levels seen across early‑2026.

The month’s strength was underpinned by a broad based rise across Residential and Infrastructure, signalling resilient pipeline conversion despite sectoral volatility elsewhere.

Residential approvals remained dominant, reaching £4.59bn, representing the single largest share of monthly value. High value approvals such as large student accommodation development at Southwark Station OSD (£200m), Achilles Estate (£125m) and Clyde Street, Digbeth (£112m) anchored monthly uplift.

Infrastructure recorded one of the strongest sectoral shifts, driven overwhelmingly by the continued acceleration of nationally significant energy projects. The month included approvals for major battery energy storage systems, hydrogen generation facilities, and multi hundred MW solar farms, with values ranging from £50m to £150m.

Education was one of weaker performers this month, falling 45%. Despite this Education is still performing at its typical scale for early year periods, with major projects generally appearing irregularly throughout the year.

Regionally, London led the month with £2.27bn of approvals, supported by an outsized concentration of high value residential redevelopment, major commercial refurbishments, and large clean energy infrastructure serving the capital’s demand profile. The East Midlands closely followed at £2.19bn, buoyed by major solar and battery storage schemes, while the South East delivered £1.19bn, underpinned by large scale housing phases and hospital estate projects.

Planning Approval Monthly Value by Sector (£bn)

No Data Found

Region Share of Approval Value by Sector (%)

No Data Found

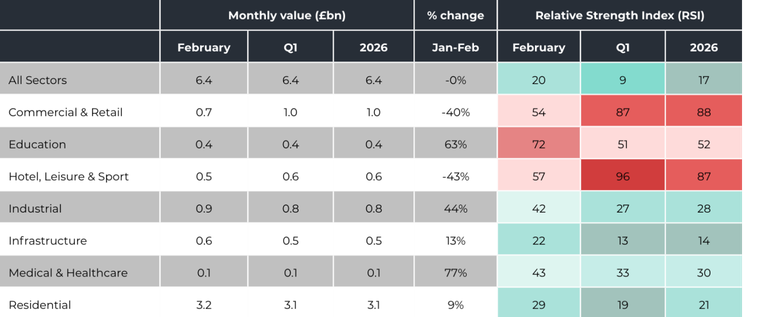

Planning Applications

Applications across all sectors totalled £6.39bn in February 2026, representing a broadly stable month‑on‑month picture following January’s seasonal softening.

Overall activity remains consistent with the late‑2025 baseline, indicating normal cyclical fluctuation rather than any material weakening in underlying demand.

Residential continued to anchor activity, contributing the largest share of total value at £3.18bn, with schemes ranging from major multi phase housing programmes to small infill developments across nearly every UK region. Although dominated by high volume schemes in the South East, East of England and North West, the sector’s broad geographical distribution highlights ongoing demand for new housing and regeneration.

Infrastructure remained a significant contributor, driven by large scale energy transition projects including solar farms, battery storage installations and hydrogen generation facilities. Key schemes such as Kinghorn Power Generation (£100m) and Kemsley Fields Hydrogen Plant (£80m) underlined the sector’s continued strategic importance and its growing share of long term capital deployment.

Medical & Healthcare activity moderated after recent peaks, consistent with the sector’s characteristic month to month volatility. While headline value fluctuated, the pipeline continues to include both large acute care redevelopments and numerous smaller clinic, care home and estate upgrade schemes across the UK, contributing to overall stability.

Regionally, the South East again led with £1.44bn in applications, supported by a strong mix of Residential, Commercial & Retail and major energy related Infrastructure submissions. The region’s largest individual project was the Newtown Railway Works Redevelopment (£250m), reinforcing its long standing dominance in large scale development activity.

The North West recorded £0.75bn, bolstered by high value industrial and residential schemes, including North Leigh Park Phase 2 (£149.1m). Meanwhile, Scotland and the East Midlands saw substantial contributions from Healthcare, Industrial and Infrastructure investments, while Wales maintained steady levels through residential and care led projects.

Planning Application Monthly Value by Sector (£bn)

No Data Found

Region Share of Application Value by Sector (%)

No Data Found

Be the first to know

A monthly snapshot of the UK construction industry covering contract awards, planning approvals, and applications by sector, featuring expert commentary and detailed data visualizations.

Want to be the first to know the latest Construction Industry Monthly Snapshot is available? Sign up to be notified.

Need a previous edition of the Snapshot?

We’ve made it easy to access recent insights. You can instantly download the last three editions of our Construction Industry Snapshot as a handy Excel file below.

Need more historical data? Our team can help you access older reports on request. Just reach out and let us know what you need, we’ll be happy to assist.

Methodology for Construction Industry Monthly Snapshot

The Construction Industry Monthly Snapshot acts as a leading indicator of current and future activity in the construction industry. All values provided are at current prices, expressed in £bn unless stated otherwise and are non-seasonally adjusted.

The RSI is an index that measures current activity levels relative to

the last 5 years. It is presented on a scale of 0-100, where:

● 0 is no activity,

● 100 is the maximum possible activity, and

● 50 is the average level of activity.

Sectors covered in the snapshot

The sectors that are included in the Construction Industry Monthly Snapshot are:

2025 Construction in Review

Our January edition of the snapshot features a review of the construction industry in 2025. This edition contains even more insight on the industry’s performance, including additional expert commentary, comprehensive data tables and concise visualisations.

Free Construction Industry Insight Reports

Barbour ABI provides construction industry insights and intelligence. Head to our Construction Market Analysis Report pages to get even more free construction insights sent straight to your inbox every month.