Construction Industry Monthly Snapshot by Barbour ABI

A monthly snapshot of the UK construction industry covering contract awards, planning approvals, and applications by sector, featuring expert commentary and detailed data visualisations.

Construction Industry Monthly Snapshot - July 2026⬇️

Contract Awards

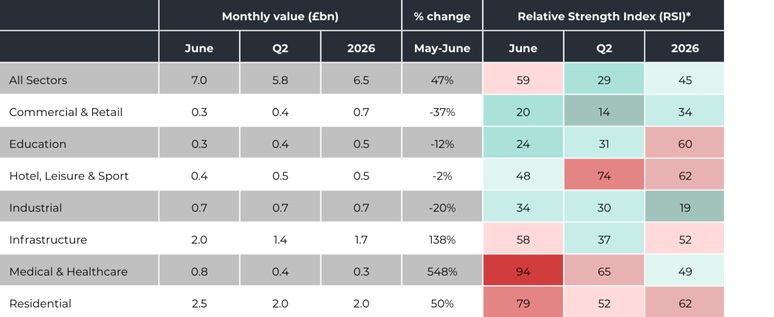

Contract awards recovered significantly in July, rising to £7bn following the weak performance seen during Q2 previously. This represents a marked improvement and suggests some previously delayed projects are now progressing to delivery.

Residential awards totalled £2.5bn, remaining the largest sector. Major projects included Wellington Square (£220m), Charing Cross Gateway Phase 1 (£135m) and several substantial student accommodation developments.

Infrastructure awards rebounded strongly to £2.0bn. The sector was supported by transport, water, rail and energy-related schemes, indicating that major public and regulated-sector investment continues to convert into live work.

July 2026 marked an improvement across the UK construction market. Although applications were poor this month, approvals and awards all strengthened simultaneously, providing encouraging evidence that the softness experienced during parts of Q2 was not developing into a broader downturn.

The month’s performance was characterised by large projects in renewable energy, data centres, healthcare, infrastructure and residential development. Data centre investment was particularly notable, reflecting the continued expansion of UK digital infrastructure and growing demand from AI, cloud and technology operators.

Infrastructure remains the industry’s most reliable growth driver, with substantial volumes progressing through both the approvals and awards stages. Energy generation, battery storage, water resilience and transport improvement projects continue to underpin market activity and provide stability against wider economic uncertainty.

Residential activity remains structurally strong. While private housebuilding continues to face challenges from financing costs and affordability constraints, the volume of approved and awarded large-scale schemes suggests developers are maintaining confidence in longer-term housing demand.

Overall, July presents a far more positive picture than seen during Q2. The combination of rising approvals and a recovery in awards suggests momentum entering the second half of 2026, although the market remains heavily reliant on major infrastructure, institutional and strategically significant projects to sustain growth.

Contract Award Monthly Value by Sector (£bn)

No Data Found

Region Share of Award Value by Sector (%)

No Data Found

Monthly Highlights

Commercial & Retail totalled £330m this month, representing a 37% decrease on last month. The largest project was a £60m mixed development at Holborn Circus.

Medical & Healthcare increased sharply to £787m, driven primarily by the £710m Jersey Hospital Redevelopment, making it the strongest healthcare month for some time.

Industrial awards reached £655m, supported by warehousing, manufacturing and specialist laboratory developments.

London dominated regional activity with £1.5bn of awards, accounting for the highest proportion of the UK total this month. The capital benefited from several of the month’s largest residential, commercial and data centre projects.

The South West also performed strongly, reaching £1.4bn, largely due to the Jersey Hospital redevelopment and a healthy mix of infrastructure and residential activity.

Planning Approvals

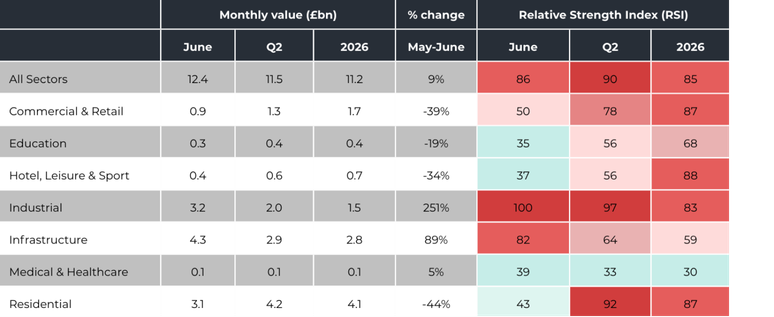

Planning approvals increased to £12.4bn in July, up from May’s already healthy £11.4bn, representing the strongest approvals performance of 2026. Unlike recent months, growth was diversified across Infrastructure, Industrial and Residential activity.

Infrastructure led all sectors at £4.3bn. Approval activity was heavily weighted towards major transport, utilities and energy projects, continuing the trend of long-term investment in nationally significant infrastructure.

Residential approvals remained robust at £3.1bn. Major schemes included the £220m Wellington Square development in Yorkshire, £135m Charing Cross Gateway in Scotland, and several large student accommodation and mixed-use developments.

Commercial & Retail delivered a healthy £900m, supported by a mix of office refurbishments, retail-led regeneration schemes and town-centre redevelopment projects.

Education and Medical & Healthcare remained comparatively modest at £312m and £112m respectively, although both sectors maintained a consistent project flow.

Yorkshire & Humber was the standout region with £3.6bn of approvals. The region was supported by several high-value residential and infrastructure projects, highlighting increasing development momentum outside the South East.

Planning Approval Monthly Value by Sector (£bn)

No Data Found

Region Share of Approval Value by Sector (%)

No Data Found

Planning Applications

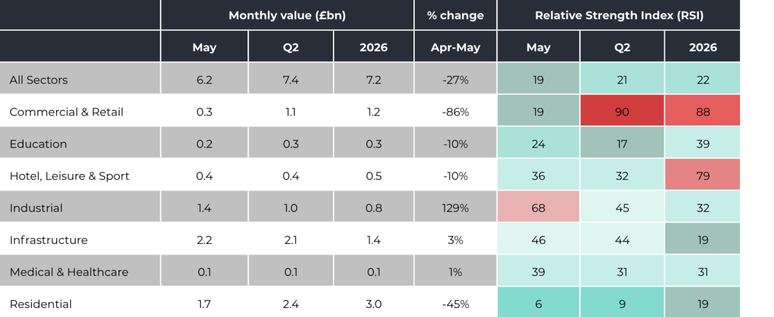

Planning applications dipped in May, falling 27% from Aprils total of £8.5bn, and down slightly on the average for 2026. Activity was driven by several major data centres and energy projects, all above £300m.

Residential saw a 45% decrease with only one major project above £100m this month. This was the lowest month for residential applications since before the start of 2025, totalling only £1.7bn. The two top projects were in the North West indicating a possible recovery in the regions.

Infrastructure was the top performing sector with a total of £2.15bn . Major projects included the Ayre Offshore Wind Farm costing £1bn and a battery storage facility at Teeside Gigapark which will cost £330m. This represents a possible recovery in the sector after a slow start to the year.

Commercial & Retail saw the largest proportional decrease, falling 86% to £270m, after a particularly strong March and April. The largest application was for a major office refurb project at 5 Aldermanbury Square in London which will cost just under £53m.

Industrial posted a strong month at £1.36bn, which represents a 129% increase on the previous month, and well above recent averages. The total is dominated though by one major project linked to Dogger bank D at a cost of £900m.

Scotland performed well on the back of the Ayre Offshore Wind farm. For all infrastructure for the UK Scotland accounted for over 50% of the UK total. The top 3 projects for Scotland were all based around renewable energy.

Planning Application Monthly Value by Sector (£bn)

No Data Found

Region Share of Application Value by Sector (%)

No Data Found

Be the first to know

A monthly snapshot of the UK construction industry covering contract awards, planning approvals, and applications by sector, featuring expert commentary and detailed data visualizations.

Want to be the first to know the latest Construction Industry Monthly Snapshot is available? Sign up to be notified.

Need a previous edition of the Snapshot?

We’ve made it easy to access recent insights. You can instantly download the last three editions of our Construction Industry Snapshot as a handy Excel file below.

Need more historical data? Our team can help you access older reports on request. Just reach out and let us know what you need, we’ll be happy to assist.

Methodology for Construction Industry Monthly Snapshot

The Construction Industry Monthly Snapshot acts as a leading indicator of current and future activity in the construction industry. All values provided are at current prices, expressed in £bn unless stated otherwise and are non-seasonally adjusted.

The RSI is an index that measures current activity levels relative to the last 5 years. It is presented on a scale of 0-100, where:

● 0 is no activity, ● 100 is the maximum possible activity, and ● 50 is the average level of activity.

Sectors covered in the snapshot

The sectors that are included in the Construction Industry Monthly Snapshot are:

Our January edition of the snapshot features a review of the construction industry in 2025. This edition contains even more insight on the industry’s performance, including additional expert commentary, comprehensive data tables and concise visualisations.

Barbour ABI provides construction industry insights and intelligence. Head to our Construction Market Analysis Report pages to get even more free construction insights sent straight to your inbox every month.