Construction Industry Monthly Snapshot by Barbour ABI

A monthly snapshot of the UK construction industry covering contract awards, planning approvals, and applications by sector, featuring expert commentary and detailed data visualisations.

Construction Industry Monthly Snapshot - August 2026⬇️

Contract Awards

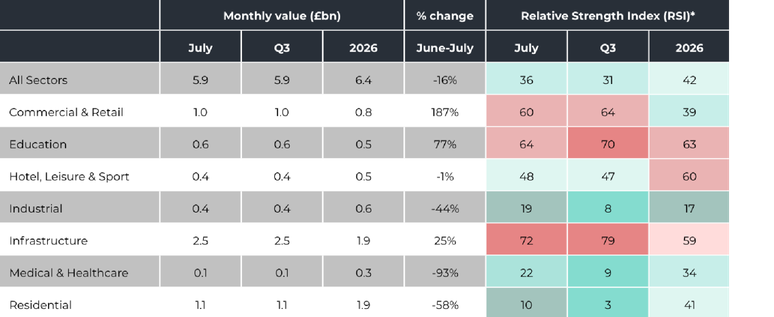

Contract awards fell 16% in July to £5.9bn with much of the value coming from large Infrastructure awards and a dip in Residential causing most of the overall dip.

Commercial & Retail increased 187% to £960m with the majority of this value coming from 3 major office developments in London.

Educations awards grew by 77% to £600m with a healthy pipeline of projects £10m and above.

Hotel, Leisure & Sport barely fluctuated at all for he third month in a row holding at £400m but still sitting about £10m below the 2025 average.

Industrial shrank by 44% to £370m, the sector’s worst performance in over 18 months. With a strong June for Industrial applications, this could turn around in the next few months.

July 2026 presented a more mixed picture for the UK construction sector than the previous month. While approvals remained robust and comfortably above long-term averages, supported by major data centre, infrastructure and renewable energy schemes, a sharp deterioration in applications raises concerns about the strength of the pipeline entering the latter part of the year. The lack of large projects progressing to application stage, particularly within Infrastructure and Industrial, suggests that developers and investors remain cautious despite healthy activity further down the project cycle.

Infrastructure continues to provide the market’s strongest source of resilience, with energy, water and digital infrastructure projects driving both approvals and awards. The growing prominence of data centres and renewable energy schemes reflects ongoing investment in the UK’s long-term economic and energy transition priorities. However, the weakness seen across Residential, Industrial and Healthcare awards highlights that growth remains uneven and heavily dependent on a relatively small number of high-value projects. The strength of water-sector awards is likely to remain supported by AMP8 investment programmes, which are generating substantial volumes of work across treatment, wastewater and network resilience schemes over the 2025-2030 period.

The wider economic and political backdrop continues to create both opportunities and challenges. Although inflationary pressures have moderated compared with previous years, financing costs remain elevated by historical standards, while ongoing concerns around public spending, labour availability, global trade tensions and supply chain uncertainty continue to influence investment decisions. At the same time, government commitments to housing delivery, infrastructure investment, energy security and planning reform should provide support to medium-term construction demand.

Overall, the market enters the second half of 2026 with approvals indicating underlying confidence, but the significant slowdown in applications serves as a warning that future activity cannot be taken for granted. The coming months will be crucial in determining whether July’s application weakness proves to be a temporary setback or the beginning of a broader slowdown in project origination.

Contract Award Monthly Value by Sector (£bn)

No Data Found

Region Share of Award Value by Sector (%)

No Data Found

Monthly Highlights

Infrastructure increased 25% to £2.45bn, the strongest month of 2026. There were 7 projects above £100m, with the top 3 awards all being on Water in the South East and North West totalling £840m.

Medical & Healthcare collapsed to its lowest month in over 18 months at £50m. No project was above £10m. The sector was equally poor for approvals suggesting these issues could continue into the near future.

Residential awards plummeted 58% to £1.1bn, the lowest value in over 18 months but near to the dip in August last year suggested at least some of this decline can be put down to a summer lull. The largest Residential development was the £150m Westwood Village – Phases 1B, 2 & 4 in Kent.

The South East saw a 130% increase in Award value, climbing to £1.5bn. The region was helped along by the £340m Oxford Sewage Treatment Works and other large Infrastructure works. Along with Wales, the South East was one of only two sectors in overall growth in July.

The North East had its worst month since April 2024, falling 67% to £110m. Only two projects sat above £10m and both of these were green energy production facilities.

Planning Approvals

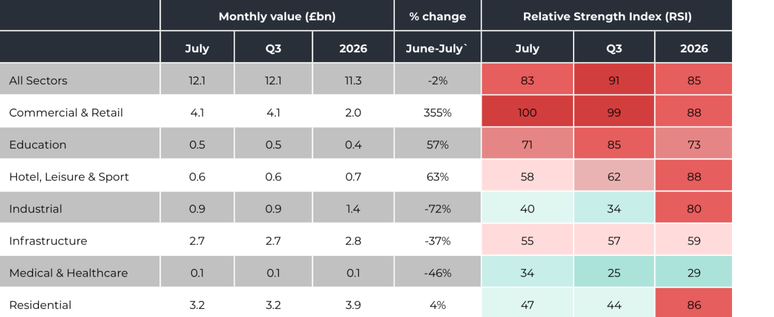

Planning approvals dipped slightly in July but remained high at £12.1bn continuing a promising 2026.

Commercial & Retail approvals led the industry at £4.1bn with a quarter of all July’s approval value coming from two large Data Centre projects.

Education approval value grew 57% to £490m with 13 projects above £10m. The largest project in this sector was the £54m Rebuilding and Refurbishment works at the Bromfords School in the East of England.

Industrial and Infrastructure approvals returned to their long running average after a bumper month in June, seemingly June was a one off and not the start of a big drive in these sectors.

Medical & Healthcare performed poorly in July dropping 46% to a disappointing £60m, with only one project above £5m.

The East Midlands saw a 77% increase in approval value in July, with over half of this value coming from the One Earth 740MW Solar Panel and Battery Storage project.

Planning Approval Monthly Value by Sector (£bn)

No Data Found

Region Share of Approval Value by Sector (%)

No Data Found

Planning Applications

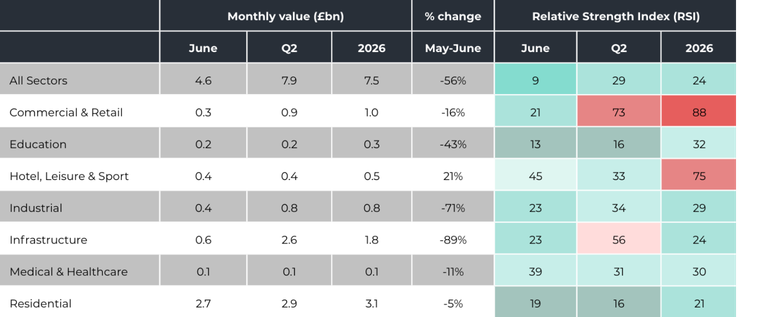

Planning applications decreased in June, 56% from May to a troubling £4.6bn. There was a striking lack of large projects, particularly in Infrastructure, with only 4 projects above £100m.

Industrial applications returned after a particularly promising May, dipping 71% to their lowest month this year.

Infrastructure applications fell by the large proportion and value, cratering to only £570m, the lowest value since November last year.

Hotel, Leisure & Sport was the only sector in growth in June, increase 21% to £400m. The sector has seen a steady and positive 2026 for applications.

Residential applications remained slightly subdued, dipping 5% to £2.7bn. The East Midlands was the only region outside London to propose an application of £100m or higher with The Springs Centre Flats and Mixed Development.

The West Midlands saw their worst performance in over 18 months with falling 54% from May to £210m.

Planning Application Monthly Value by Sector (£bn)

No Data Found

Region Share of Application Value by Sector (%)

No Data Found

Need a previous edition of the Snapshot?

We’ve made it easy to access recent insights. You can instantly download the last three editions of our Construction Industry Snapshot as a handy Excel file below.

Need more historical data? Our team can help you access older reports on request. Just reach out and let us know what you need, we’ll be happy to assist.

Methodology for Construction Industry Monthly Snapshot

The Construction Industry Monthly Snapshot acts as a leading indicator of current and future activity in the construction industry. All values provided are at current prices, expressed in £bn unless stated otherwise and are non-seasonally adjusted.

The RSI is an index that measures current activity levels relative to the last 5 years. It is presented on a scale of 0-100, where:

● 0 is no activity, ● 100 is the maximum possible activity, and ● 50 is the average level of activity.

Sectors covered in the snapshot

The sectors that are included in the Construction Industry Monthly Snapshot are:

Our January edition of the snapshot features a review of the construction industry in 2025. This edition contains even more insight on the industry’s performance, including additional expert commentary, comprehensive data tables and concise visualisations.

Barbour ABI provides construction industry insights and intelligence. Head to our Construction Market Analysis Report pages to get even more free construction insights sent straight to your inbox every month.